Here’s Why Analyst Think You Should Buy Priceline Group Inc (PCLN)

Priceline Group Inc (NASDAQ:PCLN) recently posted an excellent second quarter but the stock didn’t surge because the Street was disappointed by the guidance. However, analysts think that Priceline is an excellent investment as it remains the dominant player in the online travel bookings industry. In the second quarter, gross margins and adjusted EBITDA grew by 21% and 20% year over year, respectively. Priceline’s Booking.com platform now has over 1.3 million registered properties. Priceline’s website has 600,000 registered properties, much better than 375,000 hotels registered on the company’s top competitor Expedia . Investment firm Goldman Sachs is also bullish on Priceline. The firm has the stock on its VIP list of 2017.

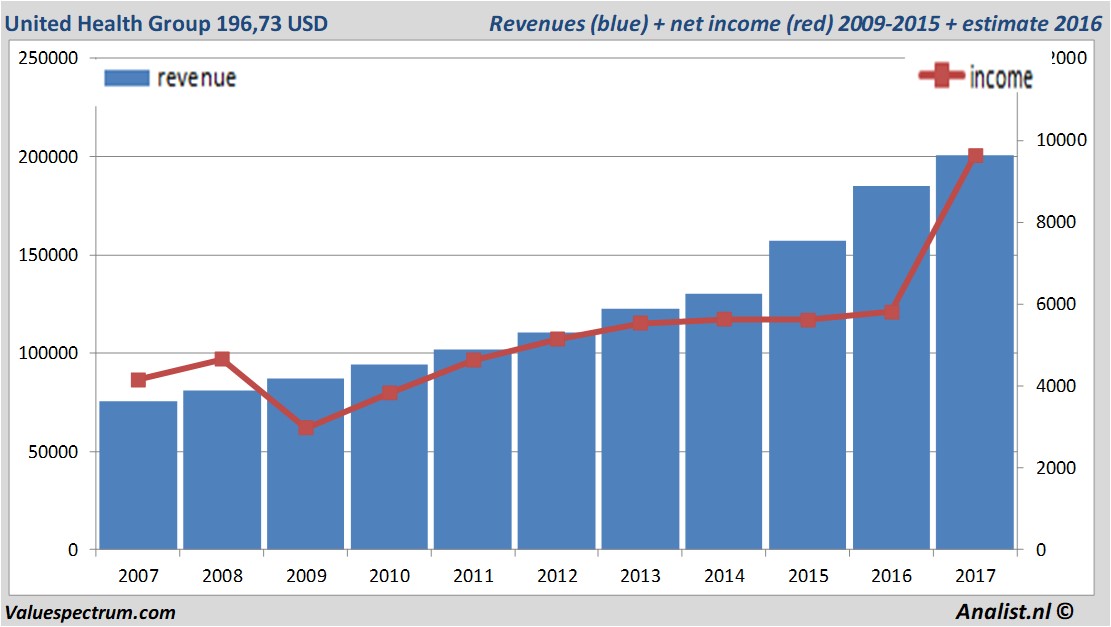

Based on the analysts' consensus: both the revenue and the net result would be on record levels. For this year United Health Group 's revenue will be around 200,51 billion USD. This is according to the average of the analysts' estimates. The expected revenue would be a record for the company. This is slightly more than 2016's revenue of 184,84 billion USD.

Historical revenues and results United Health Group plus estimates 2017

The analysts anticipate for 2017 a record net profit a 9,63 billion USD. For this year the consensus of the result per share is a profit of 9,87 USD. So the price/earnings-ratio equals 19,93.

For this year the analysts expect a dividend of 2,46 USD per share. The dividend yield is then 1,25 percent. The average dividend yield of the health care companies equals a moderate 0,20 percent.

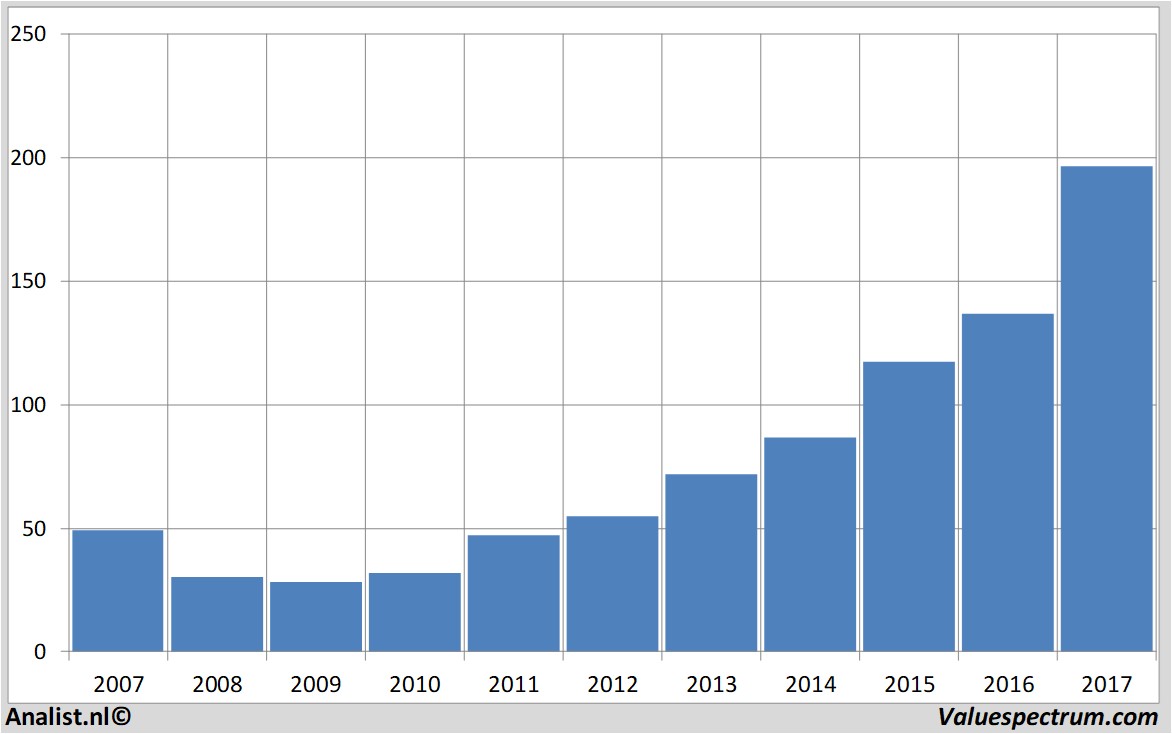

Based on the current number of shares United Health Group 's market capitalization equals 187,48 billion USD. At 15.40 the stock trades 0,58 percent lower at 196,73 USD.Price data United Health Group 2007-2017

ValueSpectrum.com News Wire & Equity Research: +31 084-0032-842

news@valuespectrum.com

Copyright analist.nl B.V.

All rights reserved. Any redistribution, duplication or archiving prohibited. analist.nl doesn't warrant the accuracy of any News Content provided and shall not be liable for any errors, inaccuracies or for any actions taken in reliance thereon.

| About us | Network | Partners |

| Fpgroup.nlinfo@analist.nlRSS feedContactIntellectual Property Photos |

Analist.nlLinksISIN

|

MorningstarPrudena.comAAII.comNASDAQvwd GroupEuronextBATS Chi-x

|