China Prepaid Card and Digital Wallet Intelligence Report 2026: A $500+ Billion Market by 2030 - Alipay, WeChat Pay and Emerging Regulated Players Such as Douyin Pay & Petal Pay Intensify Competition

Key opportunities in China's prepaid card and digital wallet market include enhancing cross-border payment solutions by integrating foreign cards into local wallets, fostering inbound tourism and commerce. Additionally, regulatory changes increase compliance and governance standards, driving innovation in card-linked wallet use. The focus on interoperability and compliance offers further growth in evolving payment landscapes.

Dublin, Feb. 27, 2026 (GLOBE NEWSWIRE) -- The "China Prepaid Card and Digital Wallet Market Intelligence and Future Growth Dynamics Databook - Q1 2026 Update" report has been added to ResearchAndMarkets.com's offering.

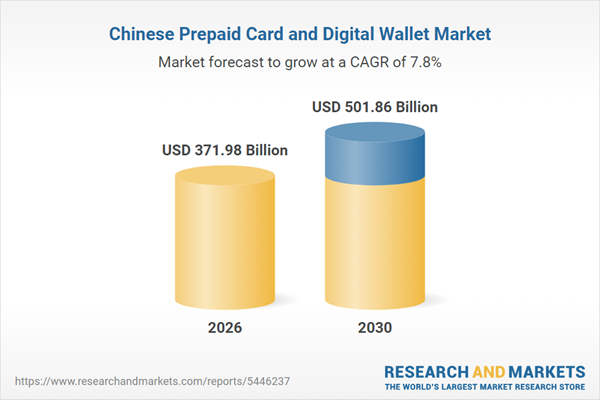

The China prepaid card and digital wallet market is expected to grow by 9.2% on annual basis to reach US$371.98 billion in 2026. The prepaid card and digital wallet market in the country has experienced robust growth during 2021-2025, achieving a CAGR of 11.3%.

This upward trajectory is expected to continue, with the market forecast to grow at a CAGR of 7.8% during 2026-2030. By the end of 2030, the prepaid card and digital wallet market is projected to expand from its 2025 value of USD 340.49 billion to approximately USD 501.86 billion.

China's prepaid-card activity sits inside a payments stack dominated by UnionPay card rails and wallet-led acceptance (Alipay, WeChat Pay). Recent momentum in "prepaid-like" usage is being pulled by inbound traveler enablement, cross-border payment connectivity, and tighter operating standards for clearing and payment institutions rather than by mass retail sale of stand-alone prepaid plastic. Some foreign apps/platforms are restricted in mainland China; market execution typically uses China-available wallet and bank channels rather than relying on restricted foreign consumer apps.

Competitive intensity should increase around compliance-grade operations and wallet-integrated usability, because both are reinforced by recent policy. The clearing-institution measures that became effective in November 2025 create a concrete compliance milestone that will influence who can scale programs and partnerships.

At the same time, inbound enablement through wallet linking will expand the addressable base for foreign networks and issuers without changing merchant behavior, which can intensify competition for travel, hospitality, and premium retail spend. Players that can combine regulated access, risk controls, and reliable wallet provisioning will gain share of the "prepaid-like" use cases.

Accelerate inbound payments by linking foreign cards into China wallets

- Inbound users increasingly pay in China by linking overseas-issued cards to local wallets, reducing the need for a separate China-issued prepaid card for short-term visitors. American Express partnered with Alipay so global American Express cardholders can link their cards to Alipay and pay at merchants across mainland China.

- China merchant acceptance is heavily wallet-led; solving inbound spend is therefore being addressed through wallet onboarding and card-linking rather than building a new prepaid distribution layer.

- Tourism and cross-border commerce priorities have kept "payment convenience for visitors" on the policy and industry agenda, creating space for wallet network integrations.

- Expect broader network coverage and more standardized onboarding for foreign cards within China wallets; this should intensify because it directly increases merchant reach without changing merchant checkout behavior.

- Prepaid will increasingly be positioned as a credential/funding layer (card-linked wallet use) instead of a visible retail product category.

Tighten the clearing governance and compliance expectations that sit underneath prepaid programs

- China has updated and reissued rules governing bank card clearing institutions, raising the operating bar for infrastructure that supports card transactions (including prepaid programs riding on these rails).

- Example: PBOC and the National Financial Regulatory Administration issued the Measures for the Administration of Bank Card Clearing Institutions (adopted April 2025; effective Nov 1, 2025).

- Regulators are tightening operational resilience, security, and governance expectations across the payment stack as volumes scale and cross-border use-cases expand.

- This aligns with a broader posture of strengthening financial stability and risk oversight in 2025.

- Operating requirements will likely become more explicit in supervision and audits post-Nov 2025; the effect will be higher compliance cost-to-serve and stronger differentiation by governance maturity.

- Program managers and issuers with weaker controls or reporting discipline will face pressure as standards are enforced.

Expand cross-border account-to-account connectivity, reshaping how prepaid supports remittance-linked use cases

- Cross-boundary payment connectivity is being built and promoted alongside card rails, changing where prepaid is needed (and where it isn't) for small-value transfers. HKMA and PBOC launched "Payment Connect Group " linking Mainland IBPS and Hong Kong FPS (launched June 2025).

- Residents' demand for low-friction cross-border remittances is being addressed via real-time bank payment system links, supported by regulators in both jurisdictions.

- As these links scale, some cross-border "top-up and spend" prepaid behaviors may shift to direct account-based transfers, while prepaid remains relevant for merchant acceptance and controlled-spend programs.

- The competitive focus moves toward interoperability and compliance (AML/CTF and settlement controls) rather than just issuing more prepaid credentials.

Formalize digital RMB (e-CNY) operational controls, influencing stored-value governance expectations

- China is tightening operational and reserve-management rules around the digital yuan, including how banks and non-bank payment institutions manage balances. Official reporting indicates non-bank payment institutions participating in e-CNY operations must maintain 100% reserves, with changes effective Jan 1, 2026.

- The objective is stronger oversight and operational clarity as e-CNY usage expands and is integrated more tightly into the financial system's measurement and control framework.

- While e-CNY is not the same product as prepaid cards, its governance model raises expectations for stored-value custody, reserve discipline, and operational controls that can spill into how issuers and payment institutions design prepaid-like balances.

- Expect continued regulatory specification and operational standard-setting rather than a rollback.

Current Market Dynamics

- China's prepaid competition is primarily shaped by how UnionPay card rails and wallet-led acceptance interact, rather than by retail shelf distribution of prepaid cards. In practice, prepaid programs compete on onboarding, token/wallet provisioning, and compliance execution in regulated institutions.

- From a supervision standpoint, the structure of licensed payment providers is relevant: the IMF notes that among licensed payment service providers, a subset conduct prepaid card issuing and acceptance, and market activity is concentrated among a small number of large players. This concentration raises the value of partnerships and regulated access paths for new entrants.

Key Players and New Entrants

- Key ecosystem anchors include China UnionPay (scheme/clearing-linked infrastructure), and the dominant wallet operators Alipay (Ant Group) and WeChat Pay/Tenpay (Tencent) that shape merchant checkout behavior. Their gravity means many prepaid propositions are effectively "distributed" through wallet experiences and bank channels rather than as standalone products.

- New-entrant momentum in the last 12 months is more visible as platform and device ecosystems obtaining or renewing regulated payment permissions, and as foreign networks pursue practical usability through partnerships. Reporting around long-term licensing highlights examples such as ByteDance's Douyin Pay and Huawei's Petal Pay being part of the regulated payments landscape, increasing competitive pressure on distribution and ecosystem bundling.

Recent Launches and Partnerships

- A major partnership pattern is international card rails connecting into China wallets for inbound usage. Reuters reported American Express joining Alipay, enabling global American Express cardholders to link and pay at merchants across mainland China.

- Separately, local tourism and municipal communications have described inbound enablement steps where foreign travelers can link international cards (e.g., Visa / Mastercard ) into China wallet environments to pay for transport and retail scenarios. These moves reduce friction for visitors and compete directly with issuing separate travel-prepaid products.

Overview of Prepaid Cards and Digital Wallet Market

Prepaid Card Market Analysis

- Metrics Assessed: The study examines the prepaid card market through various lenses, including transaction value, transaction volume, average transaction value, load value, and the total number of cards in circulation.

- Card Types: A distinction is made between open-loop and closed-loop prepaid cards, providing insights into their respective market shares and growth trajectories.

- Usage Categories: The report segments the prepaid card market into various categories such as general-purpose cards, business and administrative expense cards, travel forex cards, and meal cards.

- Business Segmentation: Further segmentation is provided based on business size and type, including small-scale businesses, mid-tier businesses, enterprise-level businesses, government entities, and retail consumers.

- Sector-Specific Applications: The analysis extends to specific sectors utilizing prepaid cards, including transit and toll payments, healthcare and wellness services, social security and other government benefit programs, fuel purchases, utilities, and more.

Digital Wallet Market Insights

- Key Segments: The digital wallet market is dissected across five primary spending categories: retail shopping, travel, entertainment and gaming, dining establishments, and recharge and bill payments.

- Performance Metrics: For each segment, the report evaluates transaction value, transaction volume, and average transaction value, offering a granular view of consumer spending behaviors.

- Retail Spend Breakdown: An in-depth analysis is provided for retail spending via digital wallets, covering categories such as food and grocery, health and beauty products, apparel and footwear, books, music and video, consumer electronics, pharmacy and wellness, gas stations, restaurants and bars, toys, kids and baby products, services, and other miscellaneous categories.

Virtual Prepaid Card Market Segmentation

- Categories Analyzed: The virtual prepaid card market is segmented into key categories, including general-purpose cards, gift cards, entertainment and gaming cards, teen and campus cards, business and administrative expense cards, payroll cards, meal cards, travel forex cards, transit and toll cards, social security and other government benefit program cards, fuel cards, utilities, and other miscellaneous categories.

- Performance Evaluation: For each category, the report assesses transaction value, providing insights into the adoption and usage patterns of virtual prepaid cards across different consumer segments.

Consumer Usage Trends

- Age Groups: Identifying usage patterns across different age demographics.

- Income Levels: Analyzing how income brackets influence prepaid card adoption and usage.

- Gender: Examining differences in usage trends between genders.

The report's research methodology is based on industry best practices. Its unbiased analysis leverages a proprietary analytics platform to offer a detailed view of emerging business and investment market opportunities.

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 159 |

| Forecast Period | 2026 - 2030 |

| Estimated Market Value (USD) in 2026 | $371.98 Billion |

| Forecasted Market Value (USD) by 2030 | $501.86 Billion |

| Compound Annual Growth Rate | 7.8% |

| Regions Covered | China |

For more information about this report visit https://www.researchandmarkets.com/r/xtko4s

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT:

CONTACT: ResearchAndMarkets.com

Laura Wood, Senior Press Manager

press@researchandmarkets.com

For E.S.T Office Hours Call 1-917-300-0470

For U.S./ CAN Toll Free Call 1-800-526-8630

For GMT Office Hours Call +353-1-416-8900

| About us | Network | Partners |

| Fpgroup.nlinfo@analist.nlRSS feedContactIntellectual Property Photos |

Analist.nlLinksISIN

|

MorningstarPrudena.comAAII.comNASDAQvwd GroupEuronextBATS Chi-x |