Clinical Laboratory Tests Outlook Report 2026: Market to Reach $225.8 Billion by 2034, Driven by Molecular and Precision Testing, Centralized Operations, and Shift Toward Value-Based Care

The Clinical Laboratory Tests Market offers key opportunities in expanding molecular diagnostics, oncology care, and infectious disease testing. Automation and AI promise to enhance efficiency and quality, while emerging point-of-care and at-home channels broaden access. Sustainability and value-based care drive innovation and partnerships.

Dublin, Nov. 17, 2025 (GLOBE NEWSWIRE) -- The "Clinical Laboratory Tests Market Outlook 2026-2034: Market Share, and Growth Analysis" report has been added to ResearchAndMarkets.com's offering.

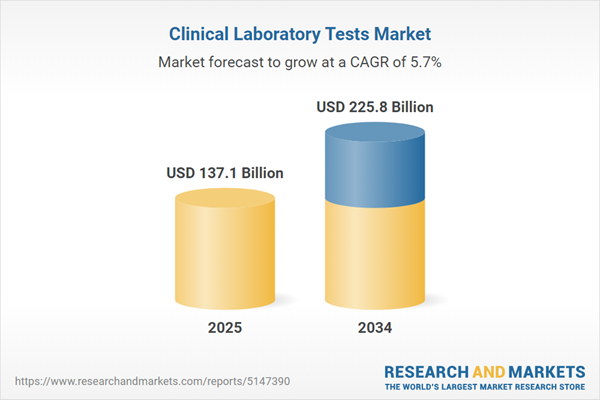

The Clinical Laboratory Tests Market is valued at USD 137.1 billion in 2025 and is projected to grow at a CAGR of 5.7% to reach USD 225.8 billion by 2034.

The clinical laboratory tests market spans routine chemistry, immunoassays, hematology/coagulation, microbiology, urinalysis, and increasingly molecular diagnostics, serving hospitals, independent reference labs, physician office labs, and emerging at-home/point-of-care channels.

Demand is propelled by aging populations, chronic disease management, infectious disease surveillance, oncology care pathways, and preventive screening programs. Laboratories are modernizing with pre-analytical automation, high-throughput analyzers, and middleware that harmonizes instruments, LIS/LIMS, and EHRs to improve turnaround time, utilization, and quality. Multiplex and syndromic molecular panels, reflex algorithms, and companion diagnostics are expanding test menus, while digital tools - analytics, AI-assisted QC, and decision support - optimize workflow and medical necessity.

Reimbursement pressure and value-based care are pushing labs to demonstrate clinical utility, consolidate volumes, and negotiate preferred networks. Health systems continue to centralize core testing while maintaining rapid response labs; independent chains leverage scale, logistics, and consumer-initiated testing portals. Data security, interoperability, and compliance remain foundational, alongside workforce strategies to offset technologist shortages. Competitive dynamics feature global IVD platform leaders, specialty niche manufacturers, and diversified service providers, with partnerships between assay developers, analyzer OEMs, and lab networks accelerating menu expansion.

Growth opportunities concentrate in molecular oncology and infectious disease, women's health, cardiometabolic risk, transplant monitoring, and pharmacogenomics, tempered by regulatory change, price compression, and supply chain resilience requirements. Sustainability initiatives - reagent waste reduction, energy-efficient analyzers, and greener consumables - are becoming procurement criteria. Overall, the market's center of gravity is shifting toward higher medical value testing, connected workflows, and patient-centric access models without compromising quality or accreditation.

Clinical Laboratory Tests Market Reginal Analysis

North America

Laboratories navigate payer policies, prior authorization, and network steerage, prompting rigorous test utilization management and outcomes evidence. Health systems intensify core-lab centralization while sustaining rapid response capability for emergency care. Consumer-initiated testing, pharmacy-based collection, and virtual care integrations broaden access, demanding robust identity, logistics, and data privacy controls. Operational priorities include workforce retention, total lab automation, and analytics-driven QC. Evolving expectations around developed tests and transparency drive investment in validation and governance. Competitive intensity remains high across national reference labs, integrated delivery networks, and specialty labs.

Europe

The region balances strong public reimbursement frameworks with budget discipline, favoring tenders that reward reliability, interoperability, and sustainability. Transition dynamics in regulatory oversight increase documentation, performance evaluation, and post-market surveillance workloads. Cross-border data exchange and e-referral programs raise the bar for interoperability and security. Consolidation of regional hubs proceeds alongside preservation of urgent care capabilities. Labs prioritize infectious disease resilience, oncology pathways, and cardiometabolic screening, while advancing automation to offset technologist shortages. Procurement increasingly weighs environmental impact, instrument uptime guarantees, and vendor service depth.

Asia-Pacific

Rapid capacity expansion spans public hospitals, private chains, and diagnostics hubs serving regional medical travel. Price sensitivity coexists with appetite for high-value menus in oncology, women's health, and infectious disease. Investment flows to high-throughput analyzers, molecular platforms, and sample logistics networks that connect secondary cities. Governments promote insurance coverage and digital health, boosting e-ordering and result integration. Local manufacturing of reagents and consumables grows, reducing import dependency. Quality accreditation and workforce training scale up to support multi-site networks and international collaborations.

Middle East & Africa

Health infrastructure programs elevate lab capability within new hospitals and specialty centers, complemented by private providers entering major urban markets. Reference testing is a blend of in-country build-out and selective outsourcing to international hubs. Infectious disease programs, maternal health, and non-communicable disease screening shape menu priorities. Point-of-care and satellite labs extend reach into underserved areas, necessitating strong connectivity and QC practices. Procurement emphasizes reliable service, training, and uptime, with incremental moves toward accreditation and data governance standards.

South & Central America

Public-private mixes define access and volumes, with modernization initiatives upgrading analyzers, middleware, and connectivity. Economic cycles influence capital planning, favoring platforms with flexible reagent economics and service terms. Infectious disease resilience, prenatal and women's health, and cardiometabolic screening anchor demand. Regional distributors and group purchasing organizations play central roles in supply continuity and pricing. Accreditation adoption grows, and labs pursue automation to counter staffing constraints and improve turnaround. Partnerships with insurers and employer health programs extend preventive testing and chronic care monitoring.

Clinical Laboratory Tests Market Key Insights

- Test-mix shifts to higher value menus. Molecular diagnostics, syndromic infectious disease panels, and oncology liquid-biopsy workflows expand, supported by reflex algorithms. Labs balance capital intensity with menu differentiation and clinical utility narratives to sustain reimbursement.

- Automation addresses throughput and staffing. End-to-end automation - track systems, auto-verification, digital QC - reduces errors and turnaround variability. Pre-analytical robotics and standardized sample handling are now core to multi-site efficiency programs.

- Analytics and AI enhance utilization. Middleware and LIS analytics flag duplicate orders, guide reflex testing, and predict instrument downtime. AI-assisted QC and anomaly detection improve release confidence and reduce manual review burden.

- Point-of-care and at-home expand access. Pharmacy clinics and remote collection broaden reach for chronic care and screening. Governance frameworks for connectivity, proficiency, and lot control are pivotal to safeguard quality outside core labs.

- Interoperability is a buying criterion. FHIR-based interfaces, cloud connectivity, and vendor-neutral middleware de-risk integration across EHRs, devices, and public health reporting, enabling cross-facility standardization and faster rollouts.

- Value-based care reshapes economics. Payers push medical-necessity policies, prior authorization, and bundled rates. Labs respond with evidence dossiers, outcomes tracking, and partnerships that tie testing to pathway adherence and total-cost reduction.

- Consolidation and network strategies continue. Health systems centralize high-complexity testing while keeping STAT capability in satellites. Independent reference labs leverage logistics, consumer portals, and employer/insurer contracts to secure volume.

- Quality and compliance intensify. Accreditation, proficiency testing, and evolving regulatory expectations for developed tests require disciplined validation, traceability, and change control across multi-site operations.

- Supply chain and sustainability matter. Dual-sourcing of reagents, regional inventory hubs, and instrument commonality mitigate disruptions. Environmental criteria - packaging, power draw, waste - enter RFP scoring and vendor scorecards.

- New commercial models emerge. Direct-to-consumer menus, subscription wellness panels, and risk-share agreements with providers align incentives. Co-development with IVD manufacturers accelerates novel menu launches in target therapeutic areas.

Your Key Takeaways from the Clinical Laboratory Tests Market Report

- Global Clinical Laboratory Tests market size and growth projections (CAGR), 2024-2034

- Impact of Russia-Ukraine, Israel-Palestine, and Hamas conflicts on Clinical Laboratory Tests trade, costs, and supply chains

- Clinical Laboratory Tests market size, share, and outlook across 5 regions and 27 countries, 2023-2034

- Clinical Laboratory Tests market size, CAGR, and market share of key products, applications, and end-user verticals, 2023-2034

- Short- and long-term Clinical Laboratory Tests market trends, drivers, restraints, and opportunities

- Porter's Five Forces analysis, technological developments, and Clinical Laboratory Tests supply chain analysis

- Clinical Laboratory Tests trade analysis, Clinical Laboratory Tests market price analysis, and Clinical Laboratory Tests supply/demand dynamics

- Profiles of 5 leading companies - overview, key strategies, financials, and products

- Latest Clinical Laboratory Tests market news and developments

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 160 |

| Forecast Period | 2025 - 2034 |

| Estimated Market Value (USD) in 2025 | $137.1 Billion |

| Forecasted Market Value (USD) by 2034 | $225.8 Billion |

| Compound Annual Growth Rate | 5.7% |

| Regions Covered | Global |

Companies Featured

- Quest Diagnostics

- Labcorp

- Sonic Healthcare

- Eurofins Scientific

- Synlab

- Unilabs

- BioReference Laboratories

- ARUP Laboratories

- Mayo Clinic Laboratories

- NeoGenomics

- SRL Diagnostics

- Metropolis Healthcare

- Thyrocare Technologies

- InVitro (K-Group)

- Cerba Healthcare

Clinical Laboratory Tests Market Segmentation

Complete Blood Count

- HGB/ HCT Testing

- Basic Metabolic Panel Testing

- BUN Creatinine Testing

- Electrolytes Testing

- HbA1c Testing

- Comprehensive Metabolic Panel Testing

- Liver Panel Testing

- Renal Panel Testing

- Lipid Panel Testing

- Cardiovascular Panel Tests

End-User

- Central Laboratories

- Primary Clinics

For more information about this report visit https://www.researchandmarkets.com/r/63oo2a

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT:

CONTACT: ResearchAndMarkets.com

Laura Wood, Senior Press Manager

press@researchandmarkets.com

For E.S.T Office Hours Call 1-917-300-0470

For U.S./ CAN Toll Free Call 1-800-526-8630

For GMT Office Hours Call +353-1-416-8900

| About us | Network | Partners |

| Fpgroup.nlinfo@analist.nlRSS feedContactIntellectual Property Photos |

Analist.nlLinksISIN

|

MorningstarPrudena.comAAII.comNASDAQvwd GroupEuronextBATS Chi-x

|